Car Insurance in Saudi Arabia: Types, Coverage & Best Providers

Saudi Arabia: Like every global automotive market, car insurance in Saudi Arabia is not a requirement; it is the law. A car without valid insurance is nothing but an illegal possession that can cost you heavy penalties, vehicle impoundment, and legal troubles. Besides, you remain financially vulnerable in the event of an accident or vehicle theft. Hence, it is non-negotiable whether you should buy insurance; rather, it is often about which type is best suited for your car. This is often determined by your lifestyle, the risk cover at the right cost, better coverage and a high claim ratio.

KEY TAKEAWAYS

How easy is it to get car insurance in Saudi Arabia in 2025?

Buying a new car or renewing a car insurance policy has become easy. You can buy through online platforms, agents, or directly from competitive providers in Saudi Arabia.What are the types of car insurance available in the market in 2025?

Two types of insurance policies are common: mandatory third-party liability and comprehensive plan.Why is insurance essential for a car?

Car insurance is a legal requirement for every car owner, as well as necessary to protect financially from accident damages, car theft or vehicle damage.Selecting the right insurance helps provide peace of mind, knowing that security is available when you need it the most, protecting you and your car. Whether you have leased vs bought the car yourself. There was a time when buying insurance was a hassle; that is no longer the case. Digital tools have simplified the process, but staying informed and comparing providers can save you money in the Kingdom.

Two options to choose from

When it comes to choosing insurance, there are primarily two types, and understanding each one serves you better in selecting the most suitable for your car.

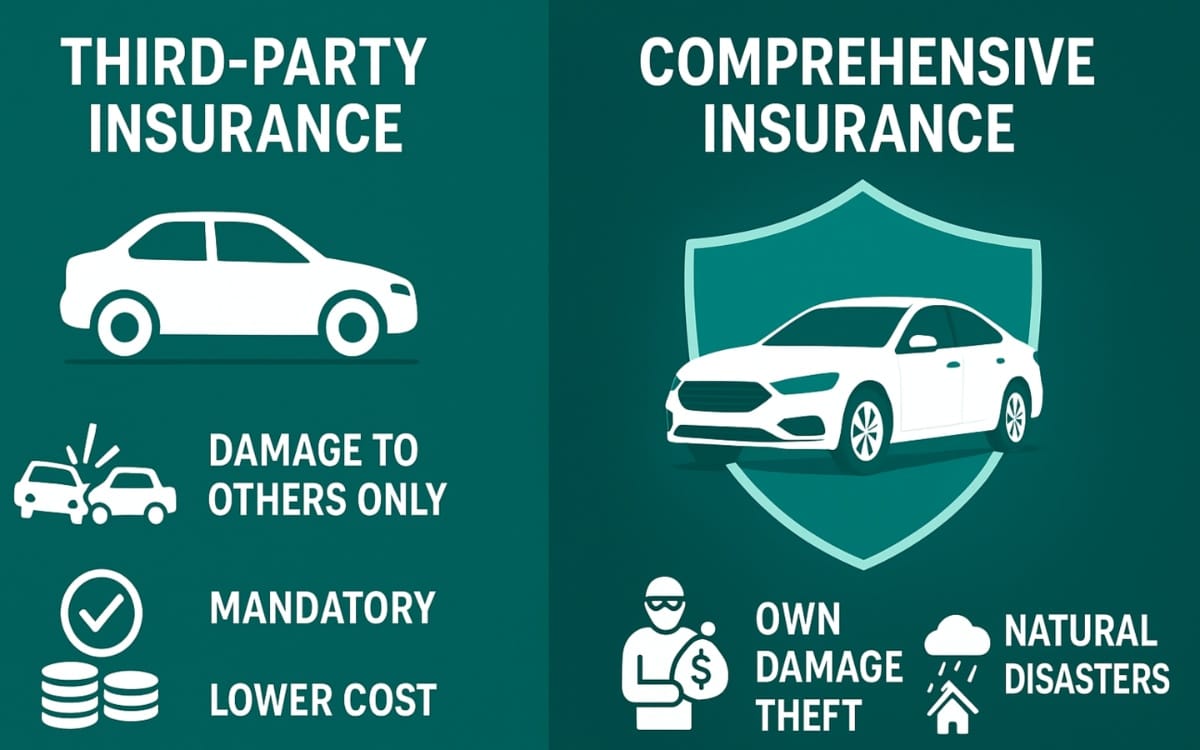

Third-Party (Mandatory)

This is the legal minimum insurance every car owner needs; there is no choice. This is mandated by law to ensure that it covers damage your car accident can cause to other people's vehicles or property. If you hit someone's car and cause SAR 50,000 in damage, third-party insurance pays for that damage. It also covers medical costs if someone is injured in an accident you caused.

Clearly, you should know that what it doesn't cover is damage to your own vehicle. Your car gets hit and destroyed? Third-party insurance doesn't pay for repairs or replacement; it is borne by the car owners.

That is precisely the reason that makes third-party insurance cheaper than comprehensive. Typically, in KSA, these insurance plans cost you between SAR 700 to SAR 1,200 annually, depending on your vehicle and driving record. It's basic protection, nothing more.

The truth is, third-party insurance is bare minimum protection. It keeps you legal. It doesn't protect your car.

|

Aspect |

Third-Party Insurance |

Comprehensive Insurance |

|

Coverage |

Damage to others only |

Own vehicle + third party + extras |

|

Legal Requirement |

Mandatory |

Optional but advised |

|

Cost (SAR/year) |

700–1,200 |

2,000–6,000 |

|

Vehicle Protection |

No |

Yes |

|

Deductible |

None |

Adjustable (250–1,000 SAR) |

|

Best For |

Older/budget vehicles |

Newer, financed cars |

|

Claims Processing |

Faster, simpler |

More thorough, longer |

Comprehensive Insurance

This is the second option when buying insurance. And as the name suggests, this is the option that actually protects you; comprehensive coverage covers damage to your own vehicle plus third-party liability. If you're in an accident, your repairs get covered. If your car is stolen, comprehensive insurance covers it. Fire, flood, hail or falling objects, pretty much everything is insured.

Since they are protecting your car from almost every possible threat, comprehensive insurance costs more than third-party. But it is worth it, because your car is probably the second-most expensive thing you own after your house, and protection is vital for your financial well-being. In KSA, the comprehensive insurance plan ranges between SAR 2,000 to SAR 6,000 annually.

You get to choose a deductible, which basically means the amount you pay when you claim. A higher deductible (say SAR 1,000) means lower premiums. A lower deductible (SAR 250) means higher premiums but less out-of-pocket when you claim. Balance your risk tolerance with your budget here. Comprehensive insurance is more suitable for a new car to cover any potential damage, as the cost of repairs is often expensive.

Factors affects premium

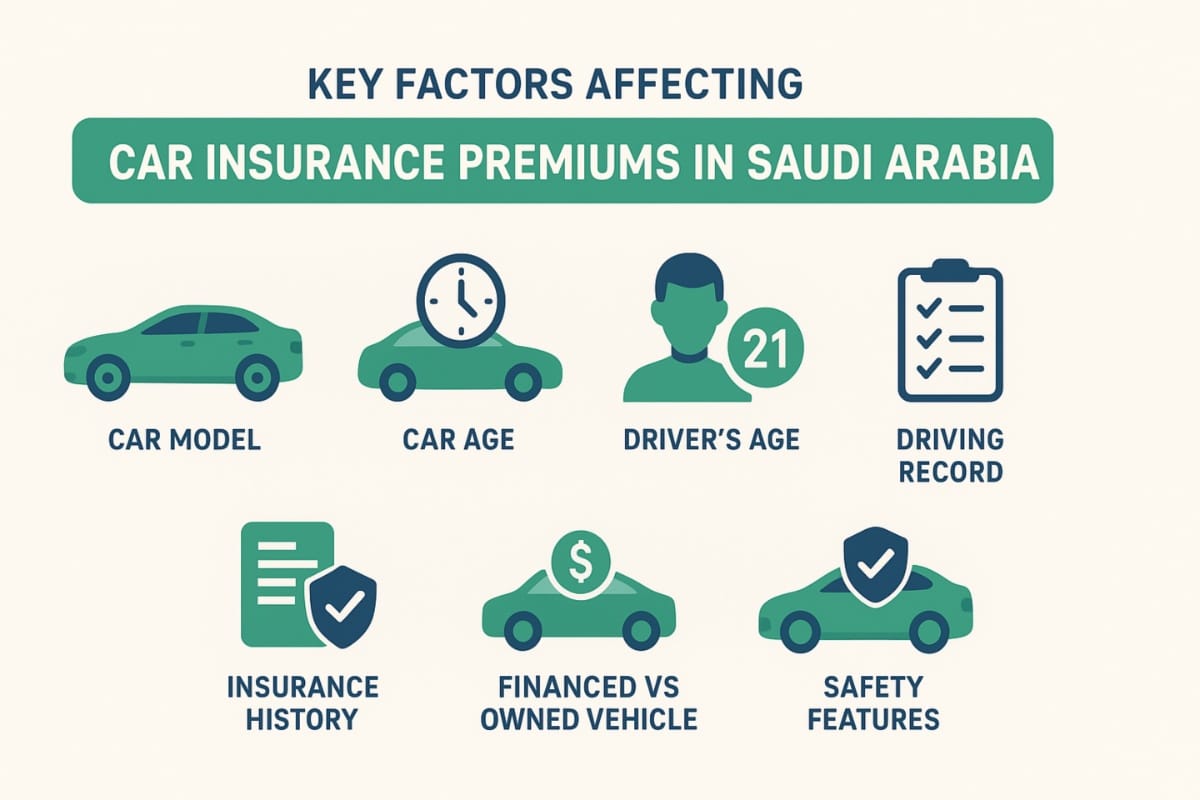

Insurance premiums are not a random amount provided by the insurance provider. They are based on several factors, which you end up paying for.

Your car's make and model matter. For example, a Toyota Corolla costs less to insure than a BMW. The reason is simple: the repair cost, the availability of parts and repair cost more. So, basically more expensive repairs mean a higher insurance risk.

Your car's age is crucial because newer cars typically cost more to insure. After all, the replacement value is higher. A 2024 car costs more than a 2015 model of the same type.

Next comes your driving record; if you follow best driving practices, most likely your premium will be lower. Accidents on your record? Your premium goes up significantly. Even for multiple violations of traffic shows on your record means your premium is most likely going up considerably.

Another key factor in determining the premium pricing is the age of the car owners. Young drivers under 25 tend to pay more. Because data proves that younger drivers often get into accidents more than older drivers. That's just the data, but even drivers over 60 years old could also face a higher premium.

The purpose the car is used for is also a big factor for a premium price. Commercial vehicles cost more to insure, as they're more often on the road and face a variety of driving conditions.

Whether your car is financed or fully paid affects coverage requirements. Financed vehicles usually require comprehensive insurance as a loan condition.

Your insurance history in Saudi Arabia is recorded. If you've claimed before, that increases your premium. No prior claims means lower risk in the insurer's eyes.

One thing that doesn't directly affect price but matters: your Iqama status. Residency permits affect insurance pricing. Some companies charge differently based on your residency status. Here is a complete guide to Car Financing in KSA Explained – Loan Types, Rates & Easiest Ways to Get Approval

Here is a complete guide to Car Financing in KSA Explained – Loan Types, Rates & Easiest Ways to Get Approval

Top Insurance Providers in Saudi Arabia

|

Top Providers |

Strengths |

Platforms/Accessibility |

|

Al Rajhi Takaful |

Wide network, competitive pricing |

Website, comparison platforms (Tameeni, Gonsure) |

|

Tawuniya Insurance |

Reliable customer service |

Comparison platforms, direct website |

|

ACIG |

Motor insurance focus, online quotes |

Branch network, website |

|

MedGulf Insurance |

Innovative packages, streamlined claims |

Website, comparison platforms |

|

Bupa Insurance |

Emphasis on customer service |

Website |

|

SAIG |

Tailored plans for individuals & corporate |

Various branches |

|

Gulf Insurance Group (GIG) |

Established with varied offerings |

Website, comparison platforms |

How to Get the Best Price

Not every insurance costs you the same as every provider has different prices and plans. You must educate yourself on key aspects of insurance. Because insurance companies compete for your business, you can use that to your advantage.

A basic start is to compare prices across multiple providers. Use comparison platforms like Tameeni, Gonsure, or visit company websites directly. Enter the same vehicle details and driving information into each platform. You'll see significant price variations. Sometimes the cheapest option is 30-40% less than the most expensive.

Increase your deductible if you can afford it. A SAR 1,000 deductible costs noticeably less than SAR 250. You're gambling that you won't claim or that claims will be minor. That gamble can save you money monthly. Bundle insurance if possible. Some companies offer discounts when you buy multiple insurance products: car, home, and health. Ask about bundle discounts.

Ask about no-claim discounts. Providers reward drivers with clean records. If it's been years since your last claim, mention it. You might qualify for discounts of 10-20%.

Consider paying annually instead of monthly. Monthly payments have administrative fees. Annual payment often costs less overall.

Some providers offer discounts for vehicle safety features. Modern cars with collision prevention systems, lane-keeping assist, or similar technology sometimes qualify for discounts.

Don't automatically choose the cheapest option. The cheapest quote isn't worthless, but it might come from a company with poor claims handling. Read reviews. Ask people who've worked with them. A SAR 200 annual savings isn't worth it if claims take months to process.

The Claims Process

Eventually, at a certain point, you may need to claim. Knowing how this works matters not just to avoid hassle but to get it done quickly and easily.

How it works in Saudi Arabia is like this. If your car gets into an accident with another vehicle, it is pertinent that both car owners go ahead and register a complaint by calling the police. And secure an official accident report. That report plays a vital role in insurance claims. Also, to secure your case with authenticity, it is better to have photos of the damage and also try to get contact information from the other driver and any witnesses.

The most important thing is to get in touch with your insurance company as early as possible after the accident. Never wait for days; reporting it right then and there helps a lot.

Most companies have hotlines for immediate reporting. And your company will assign you an adjuster. They'll inspect damage and estimate repair costs, and this process generally takes a few days.

The insurance industry works in its established way, and almost every one of them has approved repair shops. And using an approved shop makes sense as they help with faster claim settlement, something you want as your car is an affected party. You can use your own preferred shop, but be ready to wait as the claim processing takes longer.

Submit all required documentation, such as accident report, photos, police report, and repair estimates. Any incomplete documentation delays everything.

Claims processing duration is anywhere between 5-15 business days for straightforward cases, but never assume that as a standard. Sometimes, if the accident is complex, it takes a longer time

After the procedure is completed, meaning the insurance claim is approved, depending on the company, you get the payment or mostly the repair shop gets paid directly. All of this should be communicated to you upfront based on the policy and the insurance company's agreement with the repair facility.

If you're bringing a car from another country temporarily, different insurance applies for such a transaction. Najm Insurance Services handles foreign vehicle insurance through a system called “Manafith." And the insurance costs are often based on how long you're staying. A few days cost less compared to a month, and a year will take that to considerably higher. You can arrange this at border crossings or in advance through insurance brokers.

This is important if you're travelling by car from the UAE to Saudi Arabia or bringing a vehicle from another country for a short stay.

Conclusion

For every car owner, insurance in the Kingdom is mandatory by law and necessary to protect everyone involved financially. It always serves you better to choose a provider with a good claims handling reputation, not just low premiums. Make an informed decision based on actual numbers and real coverage, not just promises. Keep in mind, the purpose of insurance is to protect you financially when an unfortunate incident occurs on the road. It is always wise to never compromise on that protection. If you are a new car owner, then follow our guide on How to Buy a Used Car Safely in Saudi Arabia – Checklist & Red Flags.

Dinesh Goluguri

With over 15 years of experience in the automotive world, Dinesh Goluguri bringing hands-on experience and deep market knowledge. Passionate about SUVs, sports cars and luxury vehicles, he combines enthusiasm with expertise in delivering insights that resonate with car buyers and enthusiasts alike. With a special interest in car modifications and upgrades, Dinesh offers a unique perspective that goes beyond standard reviews, highlighting both factory features and customization potential. His work helps readers navigate new launches, features and trends in the dynamic automotive market.

Read Full Bio-

Toyota Corolla -

Toyota RAV4 2026 -

Toyota Yaris -

Toyota Raize -

Toyota Camry -

Toyota Fortuner -

Toyota Veloz -

Toyota Land Cruiser -

Toyota Crown -

Toyota Highlander -

Toyota Hilux -

Toyota Hiace

- News

- Latest

- Upcoming

- Popular

-

Toyota HiluxSAR 113,850 - 189,865

Toyota HiluxSAR 113,850 - 189,865 -

Toyota Hilux Single CabSAR 88,090 - 134,607

Toyota Hilux Single CabSAR 88,090 - 134,607 -

Toyota FortunerSAR 128,742 - 187,047

Toyota FortunerSAR 128,742 - 187,047 -

Toyota Land Cruiser 70 PickupSAR 165,025 - 201,710

Toyota Land Cruiser 70 PickupSAR 165,025 - 201,710 -

Toyota Land Cruiser HEV MAXSAR 327,290 - 334,535

Toyota Land Cruiser HEV MAXSAR 327,290 - 334,535 -

Toyota Land Cruiser 70 Hard TopSAR 158,240 - 201,192

Toyota Land Cruiser 70 Hard TopSAR 158,240 - 201,192

-

Toyota CorollaSAR 82,627 - 102,292

Toyota CorollaSAR 82,627 - 102,292 -

Toyota RAV4 2026SAR 106,662 - 165,542

Toyota RAV4 2026SAR 106,662 - 165,542 -

Toyota YarisSAR 66,700 - 78,832

Toyota YarisSAR 66,700 - 78,832 -

Toyota RaizeSAR 68,827 - 75,497

Toyota RaizeSAR 68,827 - 75,497 -

Toyota CamrySAR 109,825 - 153,985

Toyota CamrySAR 109,825 - 153,985 -

Toyota FortunerSAR 128,742 - 187,047

-

Designed for the City06 May, 2026 .

Designed for the City06 May, 2026 . -

Toyota Yaris06 May, 2026 .

Toyota Yaris06 May, 2026 . -

It shines with a completely new style06 May, 2026 .

It shines with a completely new style06 May, 2026 . -

Toyota Crown06 May, 2026 .

Toyota Crown06 May, 2026 . -

the most amazing of its generation06 May, 2026 .

the most amazing of its generation06 May, 2026 . -

Toyota Corolla Cross06 May, 2026 .

Toyota Corolla Cross06 May, 2026 . -

Toyota Rav406 May, 2026 .

Toyota Rav406 May, 2026 . -

2026 Toyota Supra Track Edition06 May, 2026 .

2026 Toyota Supra Track Edition06 May, 2026 .